23 – 27 March 2026

Weekly Trade Commentary

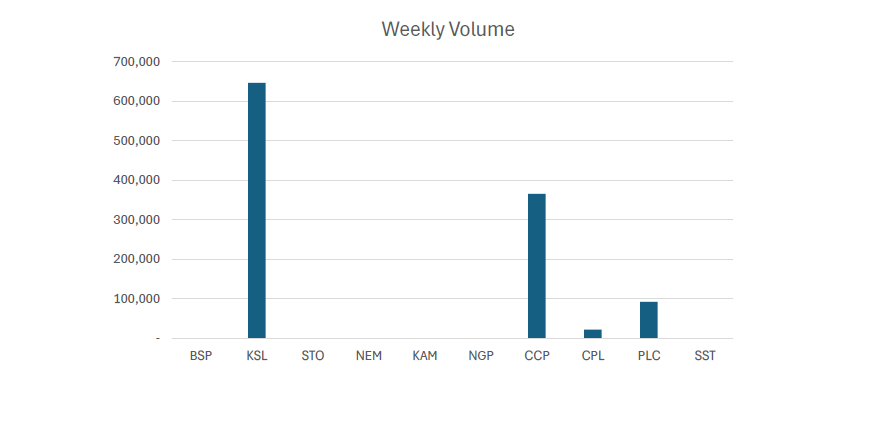

- Last week saw only 5 stocks traded on the local market with a total trading value of K4,414,704.26.

- BSP traded only 257 shares steady at K26.90.

- KSL traded 646,993 shares, closing the week steady at K3.98.

- CCP traded 365,900 shares, also steady at K4.66.

- CPL traded 21,833 shares high by 1t closing at K0.79.

- Lastly, PLC traded 92,051 units low by 2t closing the week at K1.08.

WEEKLY MARKET REPORT | 23 March, 2026 – 27 March, 2026

| STOCK | WEEKLY VOLUME | CLOSING PRICE | VALUE | BID | OFFER | CHANGE | % CHANGE |

|---|---|---|---|---|---|---|---|

| BSP | 257 | 26.90 | 6,913.30 | 26.90 | – | – | – |

| KSL | 646,993 | 3.98 | 2,586,119.66 | 3.98 | 4.00 | – | – |

| STO | – | 21.50 | – | 21.00 | – | – | – |

| NEM | – | 500.00 | – | – | – | – | – |

| KAM | – | 2.00 | – | 2.10 | – | – | – |

| NGP | – | 1.35 | – | – | – | – | – |

| CCP | 365,900 | 4.66 | 1,705,094.00 | – | – | – | – |

| CPL | 21,833 | 0.79 | 17,162.22 | – | 0.79 | 0.01 | 1.28% |

| PLC | 92,051 | 1.08 | 99,415.08 | – | 1.10 | – | – |

| SST | – | 50.00 | – | – | 50.00 | – | – |

| 1,127,034 | TOTAL | 4,414,704.26 | 0.00% |

Key takeaways:

- Market Announcement: NEM – Form 4 as filed – Peter Toth Download >>

- Market Announcement: KSL – Appointment of Deputy Chair -Richard Kimber Download >>

- Market Announcement: PLC- Results of General Meeting Download >>

- Market Announcement: PLC-Appendix 3H -Notification of Cessation of Securities Download >>

- Market Announcement: PLC- Strategic Review of Star Mountains Copper-Gold Project Download >>

- Market Announcement: BSP -Appendix 10B & Board Change Download >> Download >>

- Market Announcement: NEM Filings Download >> Download >> Download >>

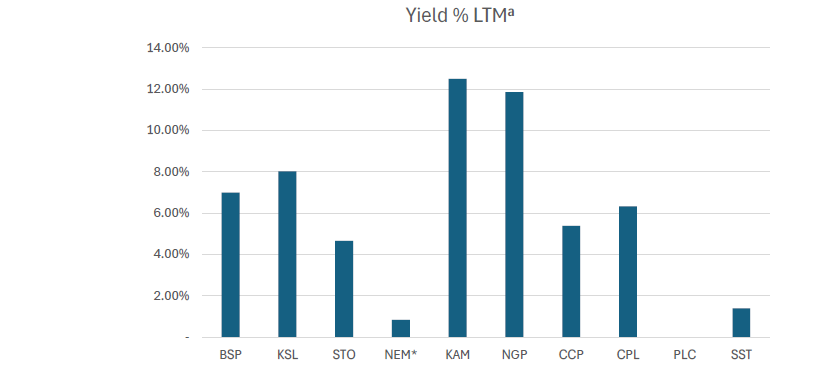

WEEKLY YIELD CHART | 23 March, 2026 – 27 March, 2026

| Stock | Number Issued of Shares | Market Cap | 2023 Interim Div | 2023 Final Div | 2024 Interim Div | 2024 Final Div | 2025 Interim Div | 2025 Final Div | Yield % LTM |

|---|---|---|---|---|---|---|---|---|---|

| BSP | 467,317,665 | 12,570,845,189 | K0.370 | K1.060 | K0.450 | K1.210 | K0.500 | K1.380 | 6.99% |

| KSL | 292,965,754 | 1,166,003,701 | K0.100 | K0.160 | K0.106 | K0.155 | K0.126 | K0.193 | 8.02% |

| STO | 3,261,616,703 | 70,124,759,115 | K0.310 | K0.660 | K0.506 | K0.414 | K0.559 | K0.443 | 4.66% |

| NEM* | 1,097,000,000 | 548,500,000,000 | – | – | – | K2.110 | K2.110 | (USD) $0.260 | 0.84% |

| KAM | 53,259,588 | 106,519,176 | K0.120 | – | K0.200 | – | K0.250 | – | 12.50% |

| NGP | 45,890,700 | 61,952,445 | K0.030 | – | K0.040 | K0.120 | K0.040 | – | 11.85% |

| CCP | 307,931,332 | 1,434,960,007 | K0.110 | K0.130 | K0.120 | K0.121 | K0.121 | K0.130 | 5.39% |

| CPL | 206,277,911 | 162,959,550 | K0.050 | – | – | – | K0.050 | – | 6.33% |

| PLC | 858,075,186 | 926,721,201 | – | – | – | – | – | – | – |

| SST | 31,008,237 | 1,550,411,850 | K0.350 | K0.600 | K0.400 | K0.300 | K0.400 | – | 1.40% |

| TOTAL | 636,605,132,233 | 5.76% |

a LTM = Last Twelve Months. We have calculated yields based on most recently declared

interim and final dividends.

* NEM pays quarterly dividends. We have added last 4 payments at current FX rates.

* NEM dividends in $USD until PGK rate is announced.

*PLC now added

Dividend yield – is calculated by dividing a company’s annual dividends per share by its current share price and expressing the result as a percentage.

INVESTOR EDUCATION

- Who do I contact if I have any questions in relation to my dividends and registration details?

– All publicly listed companies on the PNGX are required to maintain a share registry. In PNG, PNG Registries Limited and Computershare are currently the only share registry service providers for publicly listed companies on the PNGX. A share register contains information about company shares and the shareholders (members) of a company. Specifically, it details all the shares issued to shareholders and is the full history of share transactions and the ownership structure of a company.

– The share registries are responsible for maintaining an accurate shareholder record, issuing holding statements, and managing dividend payments. All information from a listed company is distributed by the share registry on its behalf to its shareholders. The share registry updates the listed company’s share register after all the trades are reported by the PNGX. In effect, the share registry will register the buyer as a new shareholder (equal to the amount purchased) and remove the seller from the share register (equal to the amount sold). If you are a buyer, the share registry will issue you with a holding statement.

The share register of the following 9 publicly listed companies on the PNGX is managed by PNG Registries Limited currently.

• BSP Financial Group (BSP)

• Credit Corporation (PNG) Limited (CCP)

• City Pharmacy Limited (CPL)

• Kina Asset Management Limited (KAM)

• Kina Securities Limited (KSL)

• NGP Agmark (NGP)

• PNG Air Limited * (Currently Suspended from Trading) *

• Niuminco Mining Limited * (Currently Suspended from Trading) *

• Pacific Lime & Cement Limited (PLC)

The share register for the following 3 publicly listed companies on the PNGX is managed by Computershare, an Australian-based share registry:

• Steamships Trading Company Limited (SST)

• Santos Limited (STO)

• Newmont Corporation (NEM)

*Only investor related queries on STO can be relayed to the PNGX office in Port Moresby.

- PNG Registries Limited

Address: PNG Registries Limited Level 4, Cuthbertson House Musgrave Street, Port Moresby, NCD

PO Box: 1265, Port Moresby, NCD

Email: pngregistries@cm.mpms.mufg.com

Tel: (675) 321 6377/78

- PNGX

Address: Office 2, Level 1, Monian Tower, Douglas Street, Port Moresby, NCD

PO Box: 1531, Port Moresby, NCD

Email: pngx@pngx.com.pg

Tel: (675) 320 1981/82

- Q. How should I update my personal information?

A. Contact the relevant share registry and inform them of any changes.

It is important that your personal information, held by the share registry, is accurate and up to date. If there are any changes to your personal information, it is your responsibility to inform the relevant share registry.

Personal Information includes:

• Name

• Signature

• Bank Account Number

• Security Reference Number (SRN)

• Contact Number

• Registered Address

The relevant share registry requires this information to send your dividend payments, holding statements or any other documents/information that the listed company, wishes, or is required to, communicate with you are its shareholder. If you need to update your personal information, please contact PNG Registries Limited, Computershare, or PNGX, depending on which shares you hold. The contact details are listed above. Note: you will need to provide identification and a copy of your holding’s statements containing your SRN (Security Reference Number) to update your personal details.

Domestic Markets Department – Money Markets Operations Unit

Auction Number: 25 MAR-26 / GOI / Government Treasury Bill

Settlement Date: 27-MAR-26

Amount on Offer: K350.000 million

| TERMS | ISSUE ID 2025 / 63 | ISSUE ID 2025 / 91 | ISSUE ID 2025 / 4741 182 | ISSUE ID 2025 / 4700 273 | ISSUE ID 2025 / 4743 364 | TOTAL |

|---|---|---|---|---|---|---|

| Weighted Average Yield | 0.000 | 0.00% | 5.43% | 5.61% | 5.63% | |

| Amount on Offer Kina Million | 0.000 | 0.000 | 30.000 | 70.000 | 250.000 | 350.000 |

| Bids Received Kina Million | 0.000 | 0.000 | 117.500 | 183.000 | 523.790 | 824.290 |

| Successful Bids Kina Million | 0.000 | 0.000 | 42.000 | 155.000 | 212.790 | 409.790 |

| Overall Auction OVER-SUBSCRIBED by | 0.000 | 0.000 | 87.500 | 113.000 | 273.790 | 474.290 |

Domestic Markets Department – Money Markets Operations Unit

Auction Number: 17-MAR-26 / GOB / Government Bond

Settlement Date: 20-MAR-26

Amount on Offer: K200.000 million

| SERIES | Amount on Offer (K’million) | Bids Received (K’million) | Successful Bids (K’million) | Successful Bids Yield | Weighted Average Rate (WAR) | Coupon Rate | Overall Auction Net Subscription |

|---|---|---|---|---|---|---|---|

| Issue ID 2026/5057 (3 years) | 30.000 | 33.45 | 23.45 | 5.75%-6.57% | 6.48% | 5.75% | K3.45 |

| Issue ID 2026/5058 (5 years) | 40.000 | 65.000 | 55.000 | 6.58%-6.89% | 6.80% | 6.00% | K25.000 |

| Issue ID 2026/5059 (7 years) | 50.000 | 68.000 | 68.000 | 6.25%-7.11% | 6.95% | 6.25% | K18.000 |

| Issue ID 2026/5060 (10 years) | 50.000 | 72.000 | 42.000 | 6.05%-7.23% | 7.14% | 6.50% | K22.000 |

| Issue ID 2026/5061 (15 years) | 30.000 | 42.000 | 12.000 | 7.46%-7.55% | 7.48% | 6.75% | K12.000 |

| TOTAL | 200.000 | 780.450 | 200.450 | K80.450 |

What we have been reading

High Debt, Hard Choices

INTERNATION MONETARY FUND

By: ERA DABLA-NORRIS & RODRIGO VALDÉS

Mounting public debt and rising interest rates are stretching finances and forcing difficult decisions.

Fiscal policy has always involved trade-offs. Whose priorities will be financed? Whose burdens will be deferred? Under what conditions? Until recently, governments could postpone these choices by borrowing on convenient terms. But now, unprecedented debt levels and higher borrowing costs have raised the stakes. At the same time, demand for public funds is growing even as resources are stretched thin. Societies can reconcile competing priorities successfully only if they depend on something often overlooked and currently in short supply: public trust.

Even before the COVID-19 pandemic, public debt was climbing steadily. In many democracies, political platforms favored higher spending and deficits while deferring structural reforms (Cao, Dabla-Norris, and Di Grigorio 2024). Modest economic growth, spending to care for a swelling elderly population, and reluctance to raise taxes just made things worse. Hard choices were put off, and debt accumulated, sustained by the unusually low interest rates of the past two decades.

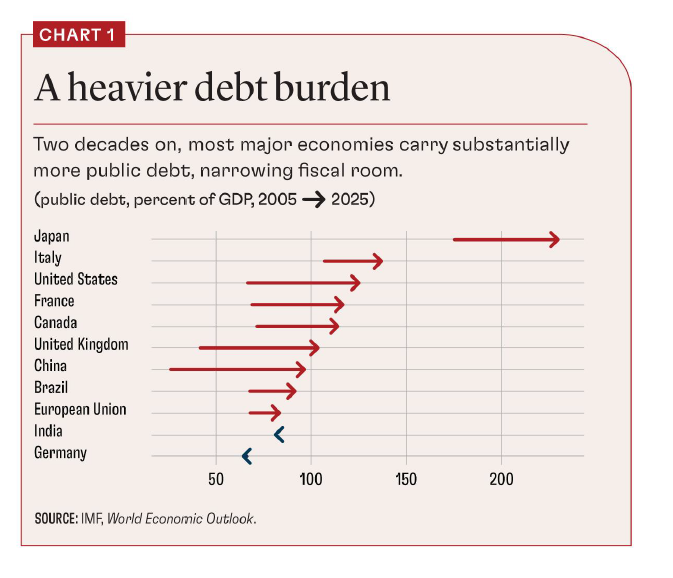

Then, in 2020, faced with the worst economic collapse since the Great Depression, governments began to borrow extensively. Advanced economy debt jumped by tens of percentage points of GDP; in some countries it exceeded 120 percent (see Chart 1). Emerging market and low-income countries, though more constrained, also borrowed heavily. The response averted a deeper catastrophe, and while debt levels have since stabilized in many cases, countries now face a world where borrowing is no longer cheap.

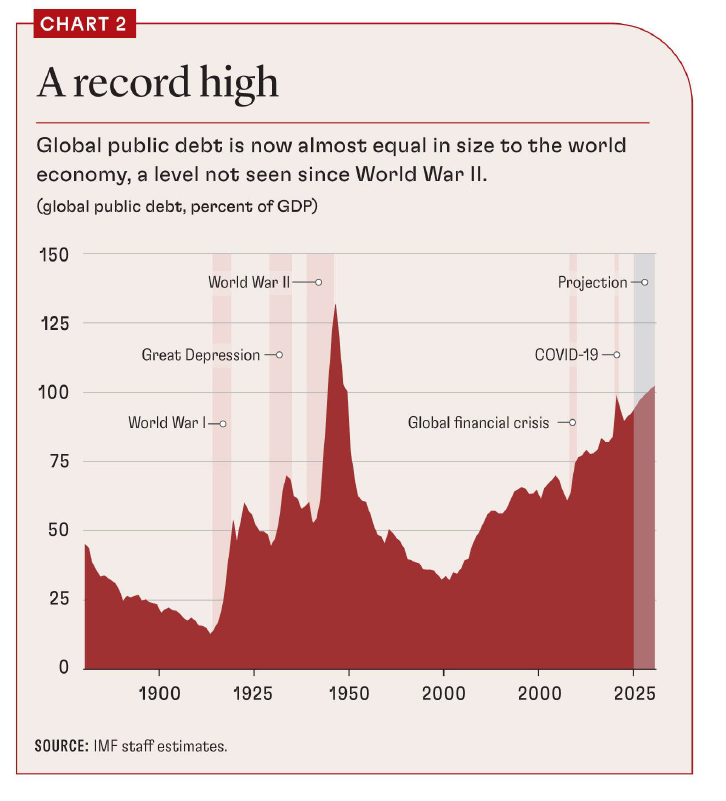

Today, policymakers face the fiscal version of long COVID—higher interest rates and rising debt costs. Global public debt climbed to 93.9 percent of GDP in 2025 and is on track to breach 100 percent by 2028—levels never seen in peacetime—marking a turning point for economic policy and politics (Chart 2). Meanwhile, long-term structural forces—aging populations, climate change, rising social demands, and, for low-income countries, declining aid flows and persistently high borrowing costs—continue to bear down on budgets even as emerging geopolitical tensions exert pressure to spend on defense and industrial policy.

Debt burden

The era of ultra-low interest rates has ended, but economic growth trends have not changed appreciably. Within a short span, borrowing costs have doubled or tripled. Interest bills now take a larger bite out of budgets, crowding out other priorities. In the US, for example, net interest payments climbed from about 2 percent of GDP before the pandemic to 4.2 percent in 2025—surpassing defense spending—and are set to rise further. In low-income countries, interest payments consume 21 percent of tax revenues on average.

High debt means less room to respond to shocks, interferes with the broader economy by raising the cost of capital, and complicates monetary policymaking while motivating financial repression. It can also threaten financial stability, especially in emerging markets, if yields rise as investors begin to doubt government’s ability to make good on its obligations. As financing conditions tighten, adjustments can become sharper and more sudden—recalling German 20th century economist Rudi Dornbusch’s insight that “crises take much longer to happen than you think, and then they happen faster than you thought they could.” And high debt shifts national income toward creditors at the expense of other needs.

In a low-debt, low-rate world, governments could sidestep hard choices by borrowing more and hoping economic growth would generate enough additional tax revenue to service and eventually repay the debt. But today, the era of easy choices is over. Every dollar a government borrows without matching revenue implies higher taxes or lower spending in the future, at least to cover the additional interest the new debt generates. Beyond a certain point, more borrowing forces painful decisions—through austerity, inflation, financial repression, or even default. The question becomes unavoidable: With limited fiscal space, what will be the trade-offs, and who will bear the cost?

Fiscal predicament

One enduring trade-off centers on the size of government. Rising living standards have led citizens to expect reliable social safety nets, affordable education and health care, robust public investment, and protection against a growing range of risks, including extreme weather and pandemics. Advanced economies greatly expanded their welfare states following World War II; many did so again after the global financial crisis of 2008 and in response to COVID-19. Emerging market economies face strong pressure to strengthen their more modest safety nets as citizens demand growth with equity. The problem is that the appetite for benefits usually exceeds societies’ willingness to mobilize revenue. And decisions to lower taxes are not always followed by spending restraint. Governments cannot provide Nordic-level benefits without Nordic-level taxation, and even with such taxes, aging and other pressures challenge the arithmetic.

Balancing credibility and flexibility poses another dilemma. Governments need room to respond to shocks, yet they must also reassure markets and citizens that debt will remain under control. Rigid fiscal rules—such as an overly binding debt ceiling—or cutting spending and raising taxes too quickly can deepen recessions, and ignoring deficits can trigger a market backlash, as happened during the euro area debt crisis. The challenge is solid commitment to sustainability without straitjacketing policy. This calls for credible medium-term fiscal anchors with escape clauses for rare shocks; transparent plans that prioritize investment while protecting the vulnerable; and institutional frameworks that build confidence without undermining the government’s capacity to respond to severe downturns. Getting this balance right has never been more important—or more difficult.

A third conundrum is whether to invest now or conserve firepower for later. Pressing needs—national security, resilience to shocks, climate transition, social inclusion, and development—demand resources. But every dollar spent today means a thinner cushion for the next crisis. In a world of frequent shocks, the trade-off is harsh. Countries that exhaust borrowing capacity in good times will find themselves dangerously exposed when the next recession or disaster strikes. It’s not about planning around best-case scenarios but designing fiscal strategies that are workable when surprises hit: It pays to hold something back when the next crisis may be just around the corner.

Each budget decision now has explicit winners, losers, and timing—and the political economy of those choices has grown more complicated. Who or what gets priority? Which taxes will fund it, and which programs must give way? These questions can no longer be papered over with new debt. They must be answered clearly, and that is proving to be a formidable challenge.

Citizens’ fears

Trust is a belief that something is safe and reliable, or that a person is good and honest. Each of these elements has a fiscal counterpart: Arrangements must be understood, fair, transparent, and competent; otherwise, they will not be trusted.

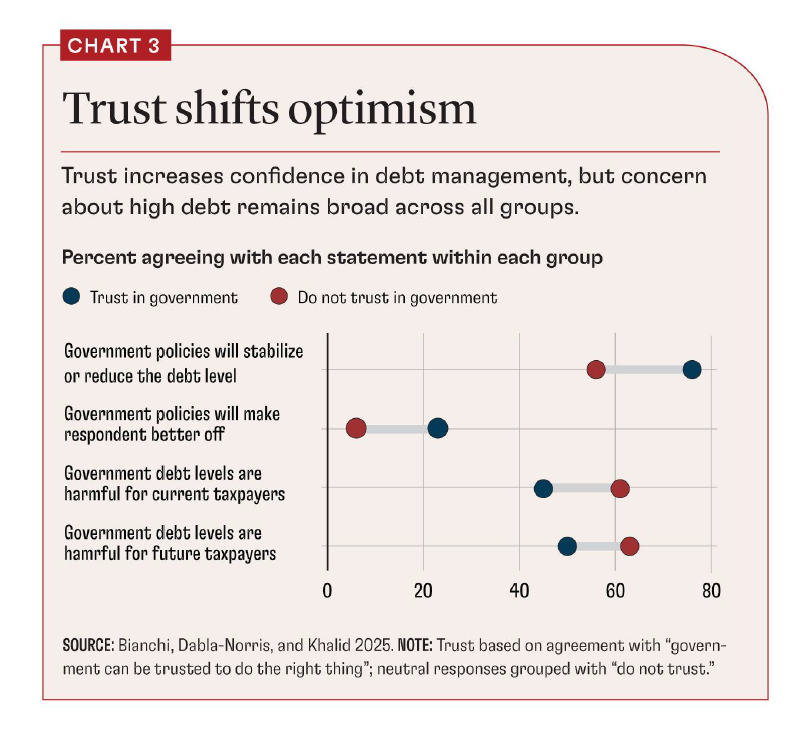

Many societies are suffering from a trust deficit (Chart 3). Recent research, based on a survey of 27,000 people in 13 countries conducted in 2024, sheds light on the gaps in perception that feed this distrust (Bianchi, Dabla-Norris, and Khalid 2025). Many people—across both advanced and emerging market economies—do not understand basic fiscal issues. For example, only about 42 percent of respondents to the survey understood that raising taxes or cutting spending would reduce a government deficit. Similarly, more than 60 percent underestimated their country’s debt-to-GDP level, especially in high-debt countries. If people believe debt isn’t that high or harmful, they will naturally view calls for fiscal reform as overblown or politically motivated. Such misperceptions blunt the sense of urgency and make it harder to build support for timely corrective action.

Without trust, pessimism about government policies rises. Respondents who report more trust in their government are 20 percent more likely to believe that its policies will help stabilize or reduce public debt. Although respondents overall tend to doubt that current policies to reduce debt will leave them better off, those with greater trust in government are 17 percent more likely to expect a positive impact on their own welfare.

The survey also revealed concerns that cut across income and demographic lines. Many people fear losing pensions or essential services they depend on. And they doubt whether the burden of fixing fiscal problems will be shared fairly. These anxieties shape how citizens vote and protest. People who expect to be hurt by fiscal reforms are far less likely to support them, regardless of the economic rationale. For instance, if middle-class workers assume that deficit reduction means a higher retirement age or a smaller pension, they will oppose it. If wealthy taxpayers suspect reform means a wealth tax aimed at them, they too will push back. And if the public thinks new taxes will be squandered through corruption or mismanagement, they will see little reason to pay them.

Experience also shapes trust. In countries that have endured repeated rounds of austerity with little to show for it, people become cynical about any new fiscal plan. If harsh cuts fail to reduce the debt, citizens understandably ask, “Why believe this next round of spending cuts or higher taxes will solve anything?” Similarly, corruption or misuse of stimulus funds undermines public confidence in government competence. In this environment, even mild reform proposals can provoke outrage, because people assume ulterior motives or unfair effects. Mention pension reform, and protests erupt when people fear their hard-earned security will vanish. Talk of tax reform, and many immediately suspect that their hard-earned income will be misused. The experience with fuel subsidy reforms is telling: The fiscal costs, poor targeting, and economic distortions are well understood, but implementation has repeatedly proved politically and socially complex.

Mistrust can spark a vicious cycle. Leaders, fearing backlash, postpone tough measures; debt problems worsen, further eroding confidence. But when citizens believe sacrifices are shared fairly and will lead to a better future, they have proved willing to accept even painful reforms—such as adjustments to pension systems (IMF 2024, 2025). Only trust will persuade voters to accept near-term sacrifices for longer-term stability.

Building trust

Today’s high public debt is testing governments and societies in unprecedented ways, and the urgent need for action is clear. Each year of drift leaves countries more exposed to interest rate shocks and shifts in market confidence. But fixing public finances is not about indiscriminate austerity. It’s about taking gradual, well-calibrated steps to put debt on a sustainable path while continuing to invest in the future. This demands honesty about trade-offs and willingness to compromise: Policymakers must level with people about hard choices, and people must recognize that some cherished programs cannot continue without additional resources or reforms.

Trust is central to this equation. People need to believe that sacrifices will be shared justly and that reforms will lead to tangible benefits. People are more likely to support difficult measures if they perceive fiscal policy as competent, transparent, and fair. But trust cannot be summoned overnight. It must be earned and sustained.

There is no single blueprint for building trust, but certain institutions and practices can help. Budget transparency and well-structured public financial management lay the groundwork. Independent fiscal councils—with clear mandates, real autonomy, and strong technical expertise, as in The Netherlands—offer impartial assessments and hold governments accountable for their fiscal plans. Spending evaluations, tax expenditure reports, and impact assessments, produced by governments or independent bodies, help both policymakers and the public understand where money is going and what it delivers. Prudent management of the public wage bill and efficient procurement can reduce perceptions of waste. Reducing special tax regimes and pension privileges enhances fairness, while strong oversight of state-owned enterprises signals responsibility and competence. Such measures are not cure-alls, but they help bridge the gap between the technically possible and the politically feasible. They create space for reform by strengthening the credibility of fiscal policy and demonstrating that governments are serious about delivering value for money.

Balancing realism about constraints with ambitions for change is essential. If we manage the debt challenge wisely, we can secure a stable foundation for long-term prosperity and preserve the social contract between generations. If we fail or wait too long, we risk economic turmoil and further erosion of faith in institutions. The fiscal path we choose today will define prosperity and fairness tomorrow.

Regards,

Benny Takin

Equities Trader

(benny.takin@jmpmarkets.com)

(+675 7001 9121/320 0240)

JMP Securities Limited

Level 3, ADF Haus, Musgrave Street

PO Box 2064

Papua New Guinea