29 June – 03 July 2026

29 June – 03 July 2026

Weekly Trade Commentary

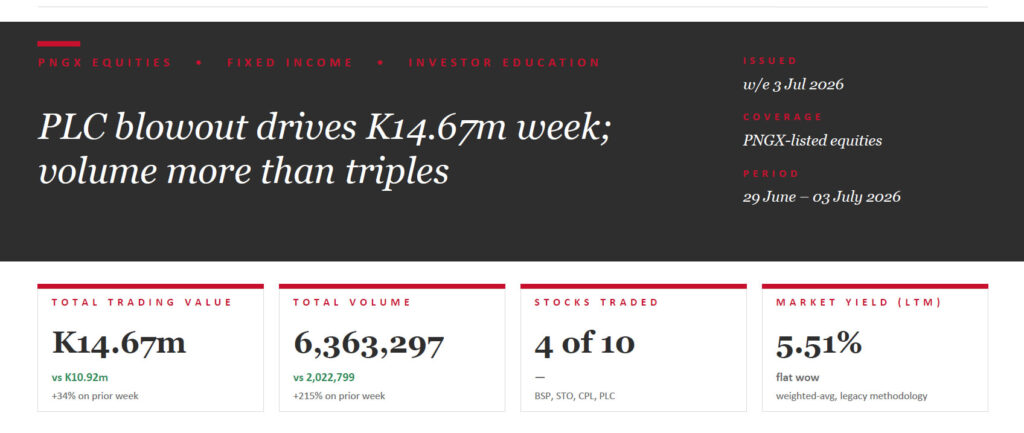

- A blockbuster week for PLC — total turnover jumped 34% to K14.67m.

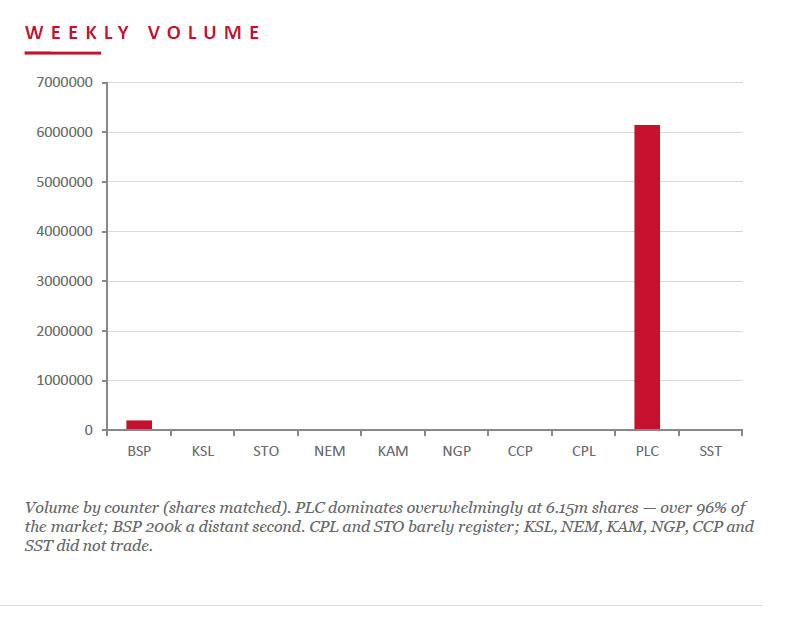

- Total volume more than tripled to 6,363,297 shares, almost entirely on one counter.

- PLC traded 6,147,495 shares, up 3t to K1.48, for K9.10m — the bulk of the market.

- BSP was the other pillar at K5.55m, easing 5t to K27.90 on 200,073 shares.

- CPL added 15,605 shares steady at K0.85.

- STO traded just 124 shares at K22.36.

- Only four counters traded — KSL and the rest sat out.

WEEKLY MARKET REPORT | 29 June, 2026 – 03 July, 2026

| STOCK | WEEKLY VOLUME | CLOSING PRICE | VALUE | CHANGE | % CHANGE |

|---|---|---|---|---|---|

| BSP | 200,073 | 27.90 | 5,552,036.70 | −0.05 | −0.18% |

| KSL | — | 4.85 | — | — | — |

| STO | 124 | 22.36 | 2,772.64 | — | — |

| NEM | — | 490.00 | — | — | — |

| KAM | — | 2.12 | — | — | — |

| NGP | — | 1.36 | — | — | — |

| CCP | — | 4.66 | — | — | — |

| CPL | 15,605 | 0.85 | 13,264.25 | — | — |

| PLC | 6,147,495 | 1.48 | 9,098,292.60 | +0.03 | +2.07% |

| SST | — | 50.00 | — | — | — |

| 6,363,297 | TOTAL | 14,666,366.19 | 0.00% |

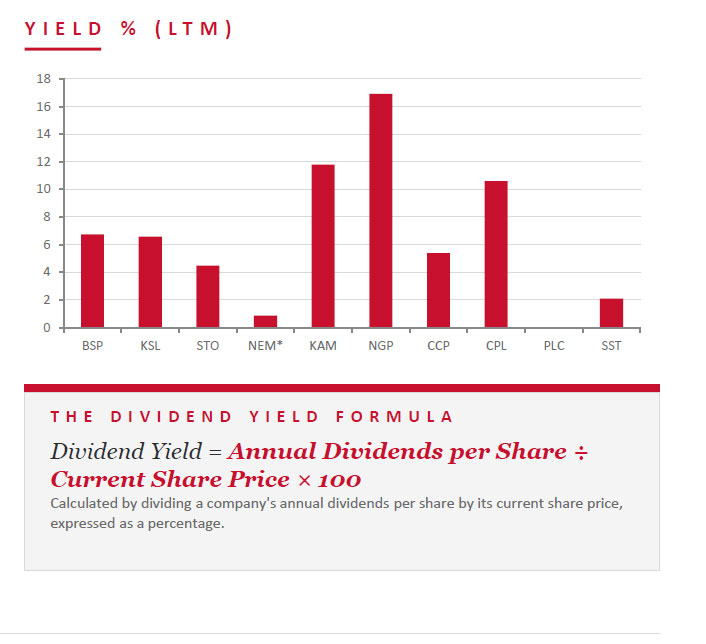

WEEKLY YIELD CHART | 29 June, 2026 – 03 July, 2026

| STOCK | ISSUED SHARES | MKT CAP (K) | INT 24 | FIN 24 | INT 25 | FIN 25 | YIELD % LTM |

|---|---|---|---|---|---|---|---|

| BSP | 467,317,665 | 13,038,162,854 | 0.450 | 1.210 | 0.500 | 1.380 | 6.74% |

| KSL | 294,332,296 | 1,427,511,636 | 0.106 | 0.155 | 0.126 | 0.193 | 6.58% |

| STO | 3,261,616,703 | 72,929,749,479 | 0.506 | 0.414 | 0.559 | 0.443 | 4.48% |

| NEM* | 1,097,000,000 | 537,530,000,000 | — | 2.110 | 2.110 | USD $0.260 | 0.86% |

| KAM | 53,259,588 | 112,910,327 | 0.200 | — | 0.250 | — | 11.79% |

| NGP | 45,890,700 | 62,411,352 | 0.040 | 0.120 | 0.040 | 0.190 | 16.91% |

| CCP | 307,931,332 | 1,434,960,007 | 0.120 | 0.121 | 0.121 | 0.130 | 5.39% |

| CPL | 206,277,911 | 175,336,224 | — | — | 0.050 | 0.040 | 10.59% |

| PLC | 860,718,662 | 1,273,863,620 | — | — | — | — | — |

| SST | 31,008,237 | 1,550,411,850 | 0.400 | 0.300 | 0.400 | 0.650 | 2.10% |

| TOTAL / WEIGHTED-AVG | 5.51% |

Key Market Announcements

- STO – Santos executes domestic Gas Sale Agreement with South Australian Government Download >>

- STO – 2025 Resource Extraction Payment Report Download >>

- NEM – Form 144 (as filed, Peter Toth) Download >>

- NEM – Second-Quarter 2026 Earnings Conference Call Download >>

BPNG TREASURY BILL AUCTION

Auction: 01-JUL-26 / GOI / Government Treasury Bill Settlement: 03-JUL-26 Amount on Offer: K270.0m (over-subscribed by K126.62m)

| TERMS | ISSUE / 63 | ISSUE / 91 | ISSUE / 182 | ISSUE / 273 | ISSUE / 364 | TOTAL |

|---|---|---|---|---|---|---|

| Weighted Avg Yield | — | — | 4.88% | 4.98% | 5.01% | — |

| Amount on Offer (K’m) | — | — | 20.00 | 50.00 | 200.00 | 270.00 |

| Bids Received (K’m) | — | — | 48.69 | 118.00 | 229.93 | 396.62 |

| Successful Bids (K’m) | — | — | 20.00 | 50.00 | 200.00 | 270.00 |

| Over / (Under) Subscribed (K’m) | — | — | +28.69 | +68.00 | +29.93 | +126.62 |

BPNG GOVERNMENT BOND AUCTION

MOST RECENT AUCTION — NO NEW ISSUANCE WEEK ENDING 3 JULY 2026

Auction: 23-JUN-26 / GOB / Government Bond Settlement: 26-JUN-26 Amount on Offer: K200.0m

| SERIES | AMOUNT ON OFFER (K’m) | BIDS RECEIVED (K’m) | SUCCESSFUL BIDS (K’m) | SUCCESSFUL YIELD | WEIGHTED AVG RATE | COUPON RATE | NET SUBSCRIPTION (K’m) |

|---|---|---|---|---|---|---|---|

| Issue ID 2026/5057 — 3 yr | 20.00 | 49.00 | 49.00 | 6.11–6.20% | 6.16% | 6.20% | +29.00 |

| Issue ID 2026/5058 — 5 yr | 50.00 | 110.50 | 72.50 | 6.30–6.43% | 6.40% | 6.60% | +60.50 |

| Issue ID 2026/5059 — 7 yr | 40.00 | 112.50 | 62.50 | 6.48–6.59% | 6.56% | 6.70% | +72.50 |

| Issue ID 2026/5060 — 10 yr | 50.00 | 55.65 | 55.65 | 6.30–6.73% | 6.72% | 6.80% | +5.65 |

| Issue ID 2026/5061 — 15 yr | 40.00 | 41.60 | 0.00 | — | — | 7.20% | +1.60 |

| TOTAL | 200.00 | 369.25 | 239.65 | +169.25 |

INVESTOR EDUCATION – Derivatives

What are Derivatives?

Derivatives are financial contracts whose value comes from an underlying asset — a stock, bond, commodity, currency or interest rate — rather than having value on their own. They serve three broad purposes: hedging risk, speculating on price moves, and arbitrage.

There are four main contract types. A forward is a private agreement to buy or sell an asset at a set price on a future date; a future is the exchange-traded, standardised version, marked to market daily. An option gives the buyer the right — not the obligation — to buy (call) or sell (put) at a set strike, for a premium. A swap exchanges cash flows, most often fixed-rate for floating-rate interest.

Who uses them? Hedgers — an airline locking in fuel, an exporter hedging currency, a manager buying puts as insurance; speculators taking leveraged directional bets; and arbitrageurs exploiting price gaps between a derivative and its underlying, which helps keep markets efficiently priced.

- Leverage risk — Small moves in the underlying can produce outsized gains or losses relative to the capital posted — the double-edged sword of derivatives.

- Counterparty risk — Mainly an over-the-counter concern: without a clearinghouse guarantee, you depend on the other side honouring the contract.

- Liquidity risk — Some OTC or exotic contracts can be hard to exit before expiry, leaving a position stuck exactly when it most needs to move.

- Complexity & model risk — Exotic derivatives can be mispriced when the underlying assumptions break down — as mortgage-backed derivatives showed in the 2008 financial crisis.

What we’ve been reading

Tokenisation could reshape the world’s financial architecture

IMF Blog • Tobias Adrian, Financial Counsellor

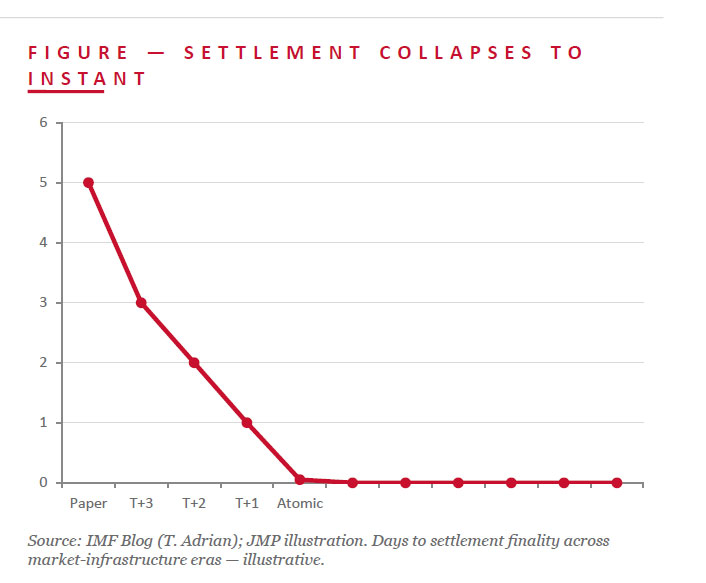

Tokenisation is usually pitched as a technical upgrade — faster settlement, cheaper payments, programmable assets. But it is more than that. When financial assets and liabilities move onto shared digital ledgers, the structure of the system itself changes: execution, clearing and settlement, which happen sequentially today, can occur simultaneously, governed by software rather than institutions.

That removes frictions — but also the buffers those frictions provide. Delayed settlement and reconciliation add cost and time, yet they also create room to intervene in moments of stress. With tokenisation, liquidity demands materialise in real time, collateral calls can be automated, and failures can propagate faster than supervisors can respond. Risk migrates from institutions’ balance sheets toward the platforms and code that govern transactions.

JMP read: For PNG and other emerging markets the IMF sees a genuine prize — faster, cheaper cross-border payments and better market access — but also real hazards: near-instant capital flight, rapid currency substitution and eroded monetary sovereignty, especially if global stablecoins take hold. The lesson: strong domestic frameworks and international coordination, not the technology alone, will decide whether tokenisation helps or fragments the system.

Regards,

Benny Takin

Equities Trader — Primary contact, JMP Weekly Report

benny.takin@jmpmarkets.com

+675 7001 9121 / 320 0240

JMP Securities Limited

Level 3, ADF Haus, Musgrave Street

PO Box 2064, Port Moresby NCD, Papua New Guinea